Mortgage Applications Decline: What It Means for Homebuyers

Introduction

After a five-week streak of growth, mortgage applications took a slight dip last week, signaling the early arrival of the winter housing market. The Mortgage Bankers Association (MBA) reported a 0.7% decline in its Market Composite Index for the week ending December 13, as rising mortgage rates tempered demand.

This shift highlights the ongoing challenges and opportunities in today’s housing market. Whether you’re a first-time buyer, a homeowner considering refinancing, or simply interested in market trends, here’s what you need to know.

Key Trends in Mortgage Applications

1. Rising Mortgage Rates

- The average effective rate for 30-year fixed-rate conforming mortgages climbed to 6.75%, an increase of eight basis points from the previous week.

- Rates for jumbo loans (6.86%), 15-year fixed-rate mortgages (6.15%), and FHA loans (6.49%) also ticked up.

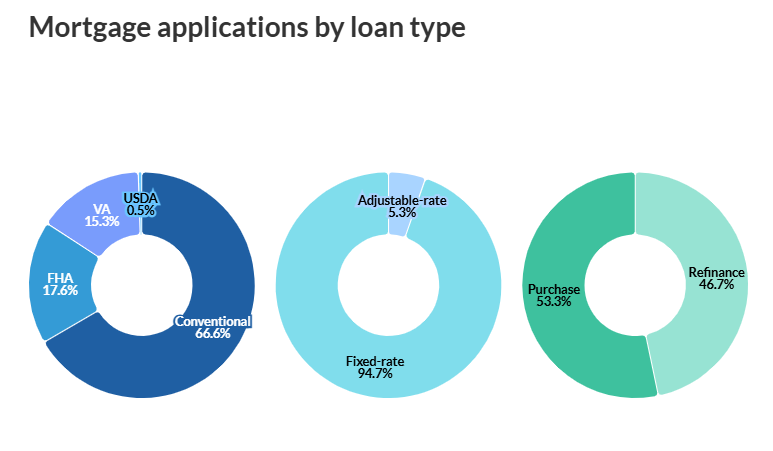

2. Purchase Applications Hold Steady

Despite rising rates, purchase applications increased by 1% as buyers took advantage of gradually improving inventory and optimism about the economy and job market.

3. Refinance Activity Declines

- The Refinance Index fell by 3%, driven by a slowdown in Department of Veterans Affairs (VA) refinance activity, which had spiked by 85% the previous week.

- Despite the weekly drop, refinance activity is still up 41% compared to the same period last year, showing long-term resilience.

4. Government Adjustable-Rate Mortgages (ARMs) Surge

- Interest in Government ARMs increased significantly, with the index up 24.1% weekly.

- The effective rate for 5/1 ARMs also rose by over 20 basis points to 6.03%, reflecting growing demand for adjustable-rate options.

What’s Driving These Trends?

1. Rate Instability and the Federal Reserve

The Federal Reserve’s monetary policy has been a major driver of mortgage rate fluctuations.

- The Federal Open Market Committee (FOMC) is expected to weigh another rate cut soon, which could stabilize rates in the coming months.

- Earlier this year, the Fed’s actions led to both rate declines and volatility, impacting affordability and demand.

2. Seasonal Slowdown

The winter housing market often sees less activity, as buyers and sellers take a step back during the holiday season. However, this year’s market is still influenced by improving inventory and strong economic fundamentals, keeping buyers active.

What Does This Mean for You?

For Homebuyers:

- Stay Ready: While rates are slightly higher, improving inventory offers more choices. Work with a mortgage professional to explore financing options like adjustable-rate mortgages (ARMs), which can provide lower initial rates.

- Act Quickly: With rates fluctuating, timing your purchase strategically can help you lock in favorable terms.

For Homeowners Considering Refinancing:

- Evaluate Your Options: Even with a weekly decline, refinancing activity remains significantly higher than last year. If you haven’t explored refinancing yet, now may be a good time to crunch the numbers.

For General Market Watchers:

- Expect Volatility: Mortgage rates may remain unpredictable as the Fed considers additional rate cuts and inflation persists.

- Stay Informed: Trends in mortgage applications can provide valuable insights into broader economic conditions, including consumer confidence and housing affordability.

Conclusion

The recent decline in mortgage applications reflects both seasonal trends and the broader impact of rising rates. For homebuyers and homeowners alike, understanding these dynamics is key to making informed decisions in today’s housing market.

While the winter slowdown may be here, opportunities still exist—especially for those who stay prepared and adaptable. Whether you’re buying, refinancing, or simply observing, keep an eye on mortgage rates and inventory trends as the market continues to evolve.